Selling to those who can't pay: human cost of modern banking

From Kotak Mahindra Bank to Justdial and Extramarks, the Mitras got caught in a web of misselling. The more they tried to break free, the more they got sucked right in

In the industrial suburb of Sarjapur in Bengaluru, 47-year-old Ram Mitra (name changed) runs a 10X10ft carpentry workshop. The shop sits precariously on an encroached footpath. It does not get too many visitors. There is one three-legged stool. Everything in the shop is movable except for a fixture atop which sits a small shrine. Almost a metaphor for the one thing he holds on to—faith. Ram Mitra was also, until recently, the owner of a Kotak Mahindra Bank credit card.

A card he was sold with the promise of “paying later”. That Mitra was approached for a credit card despite low savings is in itself astonishing. Even at his financial best, he earned Rs 20,000 ($279) a month, with his household income under Rs 30,000 ($418)—not a number banks would traditionally swoop down to offer credit cards for.

But Mitra and his family’s history with banks has been nothing short of traumatic.

Speaking about the Kotak representative, he says, “He could not even speak in Hindi, I didn’t understand what they told me”. But he understood what the card could do. “I could buy now, pay later.”

When the card came his way, his expenses were soaring and earnings were unpredictable. The Mitras were ready to grasp at any option that helped them defer payments.

Except the card bled them dry.

“We kept repaying what we thought we spent, but how much ever we repaid the balance amount did not reduce at all.” They spent nearly Rs 41,000 ($571) using the card, Mitra’s bank statements—as of September 2019—show. But, in February 2019, they got a message saying dues worth Rs 31,237 ($435) on credit card payments were pending. Six months later, another message calling for dues of Rs 5,800 ($81) dropped.

Selling to those who can’t pay: human cost of modern banking

“Only when we went to pay that due and close the credit card, we realised that credit cards have an interest payment and penalty after 45 days,” says Mitra’s wife, who works as a household help. “A friend told us we could pay back a credit card payment over one year,” she adds. The couple paid the dues partly by borrowing money from the households they work in and by taking money from another lender by pledging gold. (In an earlier story, we wrote about fintechs leaning on credit cards.)

The family’s banking woes don’t stop at credit cards or even Kotak Mahindra for that matter. While Kotak upsold products to the family—from savings to current to life insurance, a minor account, all the way up to the credit card—each time bringing financial losses to the Mitras, they’ve also suffered the ill-practice of misselling at the hands of representatives of big brands such as local search platform Justdial, Vijaya Bank and tuition app Extramarks.

Selling to those who can’t pay: human cost of modern banking

Put together, the Mitras’ misfortune from misselling amounts to Rs 4.12 lakh ($5,740) in 3 years. All emanating from a need for upward mobility and for their children to have access to a good education.

“I know how education can change lives. I wanted to study more, but I couldn’t because we were poor,” says Mitra’s wife, who studied till Class X. Their daughter, who is studying commerce, wants to do an MBA. Their son goes to a private school. Because English. “Speaking good English is important to get a good job, a government school where he’ll learn Kannada won’t be useful outside Bangalore,” she says.

Selling to those who can’t pay: human cost of modern banking

Except, schooling meant signing up for more expenditures. Out of money they didn’t have.

It’s a disease.

Those in the mass segment like the Mitras, straddled between the lower-income and middle-class households, are the most vulnerable to this disease of misselling. The lower-income segment comes under various government schemes and servicing them is almost a social duty for banks. The middle class and upper class—those who earn over Rs 6 lakh ($8360) a year—are for whom most banking products are designed. Even if mis-sold, they have the resources to fight it out. But that’s not true for the mass segment. As a result, the financial assault is relentless.

Misselling is also under-tracked. The RBI, in its Ombudsman report for 2018, got only 163,590 consumer complaints overall. The report does not even have categories to report a product-wise mis-sale. The report says only 0.4% of complainants alleged misselling. As a result, as the financial daily Mint’s consulting editor Monika Halan says in her piece if one were to go by the RBI’s report, there is no misselling by banks.

Charge sheet

RBI said 5% of the total complaints were related to levying charges without notice. These charges include non-maintenance of minimum balance, processing fees, pre-payment penalties

The Mitra’s losses are institutionally invisibilised.

Blow after blow

“A product like a credit card makes perfect sense for low-income households as they experience short term liquidity constraints and need quick access to low-cost funds for very short periods,” argues Deepti George of Dvara Research, a policy research institution. But in the current reality, it’s treated as an elite product.

Mitra, today, earns Rs 10,000 ($140) some months, Rs 5,000 ($70) in others, and some months, nothing at all. His wife makes Rs 13,000 ($180) a month.

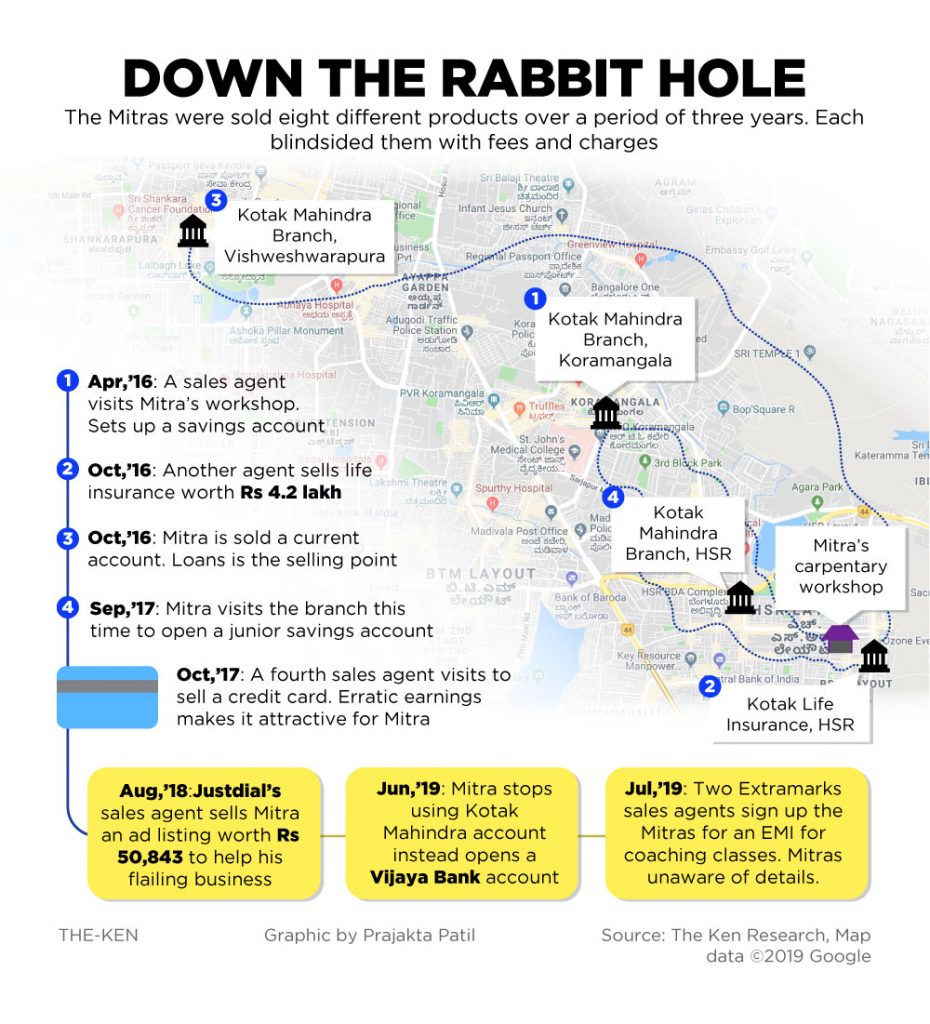

Mitra didn’t start where he is today. In 2016, he had a carpentry business that was looking up; he went from an apprentice to an entrepreneur employing 10-14 people. He had a workshop in the up-and-coming neighbourhood of HSR Layout, Bengaluru.

That’s when the first of many blows to come hit the Mitras—the savings account.

Selling to those who can’t pay: human cost of modern banking

In April that year, a salesperson came from Kotak Mahindra. A snazzy bank he associated with the affluent. Suddenly, he found himself being approached by a bank rep, instead of having to repeatedly knock on bank doors. Mitra had, back in West Bengal, made many failed attempts to get loans for a business selling puffed rice. In fact, the family moved to Bengaluru to repay a debt of Rs 10 lakh ($14,000) they owed suppliers.

Life had done a 180, Mitra thought.

Kotak, as he saw it, was also an upgrade from the government-owned Bank of India account he had. Moreover, the…

Kotak, as he saw it, was also an upgrade from the government-owned Bank of India account he had. Moreover, the bank agent promised easy access to loans. He was sold.

“The business was growing. I thought it would be useful to have an option to get a loan, and it was a big bank, so I took the account,” says Mitra.

This was a time when his business would make Rs 4-5 lakh ($5,500-7,000) in turnover, leaving him with earnings of about Rs 20,000 ($280) a month. That along with the roughly Rs 8,000 ($111) his wife earned as a household help meant they could square away savings to keep in a savings bank account whenever they saved enough.

But savings accounts are gateway products for banks. You’ll take it because of the interest on deposits. Now, the banks have your data. You become easy to sell to.

Selling to those who can’t pay: human cost of modern banking

Mitra wanted to get the most out of his savings account. He made deposits close to Rs 1 lakh for the first few months. In September, just five months after the savings account, Mitra found himself hosting a Kotak representative, who’d come down from a branch 13 km away.

Again, the bank representative dangled the loans carrot. The item on sale? A current account.

The savings account gave Mitra the confidence to handle another Kotak product. With this came a debit card—Mitra could withdraw as much money as he wanted, promised the bank representative. For a business run on cash payments, this seemed useful to Mitra.

Convenience costs

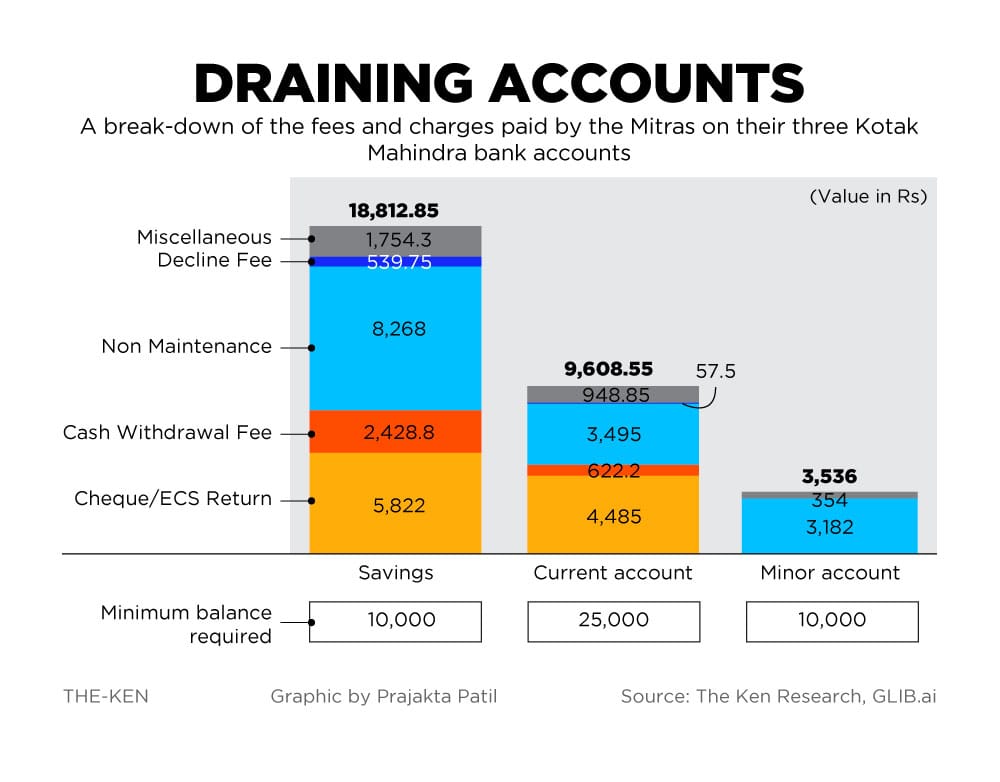

Banks offer 5 withdrawals from their own ATMs. Only 3 free withdrawals on other banks’ ATMs as it pays a fee of Rs 15 when its users use other ATMs. Mitra’s ATM cash withdrawal charges alone came to Rs 2,428, averaging Rs 23 per withdrawal in the 2.5 years he had an account

Except, the current account was a wrong sell. “Current account is meant for businesses that have a high velocity of digital payments. It earns no interest,” said a senior executive who works at a financial marketplace. “So a savings account should have been good enough for Mitra, given that he makes most of his payments in cash,” he added.

With the two accounts, Kotak agents had now signed him up for a commitment. An average monthly balance for Rs 35,000 ($500) between the two—Rs 7,000 ($100) more than the couple’s monthly income. Failing this, Mitra would be automatically charged a fee for non-maintenance. The second blow.

Banks ended up charging Mitra for non-maintenance. The irony of having a savings bank account struck them. “We thought we could save money by keeping money there, but whatever money we kept in there simply kept disappearing,” says Mitra’s wife.

But that came later.

At this point, sales agents were only starting to swarm around the Mitras.

Selling to those who can’t pay: human cost of modern banking

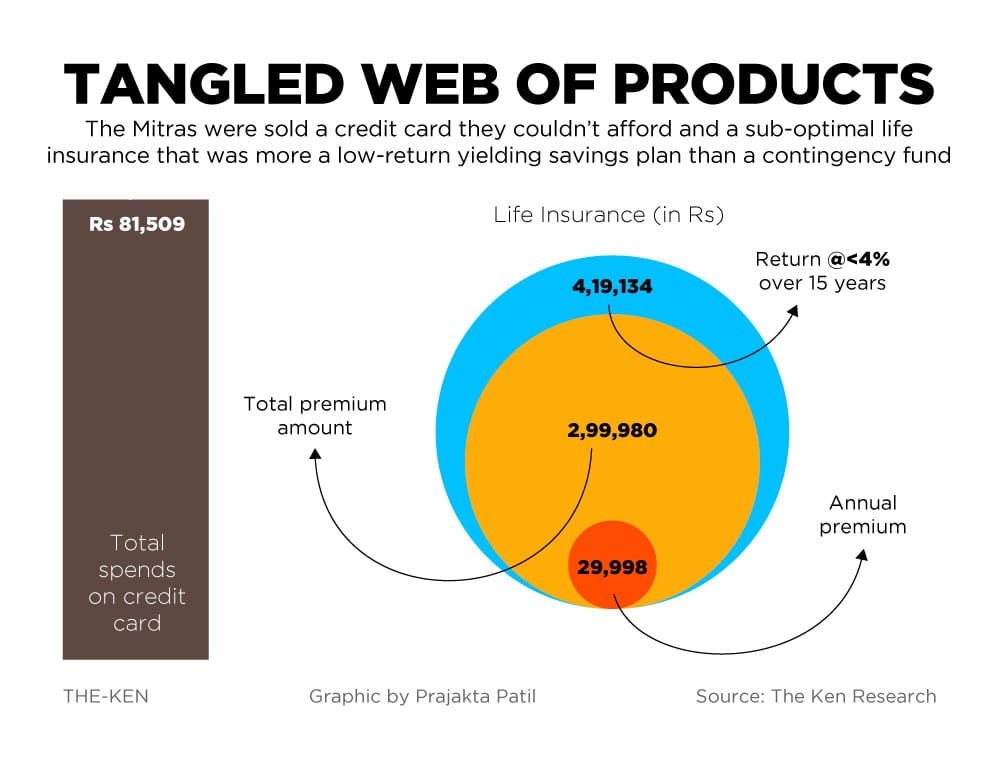

A month after the current account, the agents had a bigger promise to offer—life insurance with a cover for Rs 4.2 lakh.

For Mitra this was not just an upgrade, but a shot at a secure future, even though the annual premium of Rs 30,000 was daunting. “Why would I not take the chance to make sure my family will be fine even after my time?” he asks.

With his Kotak savings account, he could make quarterly payments. But what if he defaulted and the policy lapsed? We can’t have that, said the agent, before getting Mitra to sign a form that authorised Kotak Life Insurance to automatically debit his account every quarter.

Except the plan he was sold would only yield a return of less than 4% over 15 years, said the executive who works at a financial marketplace who reviewed the plan. This while Kotak Mahindra earns a 30%-50% commission in the first year, and a small portion through the decade Mitra makes his payments, according to the executive quoted above. Third blow.

This is where the Mitras’ problems compounded.

Neck deep

In November 2016, the Indian Rupee was demonetised, and overnight, the government banned 86% of cash. Suddenly, Mitra had no cash to make payments to his labourers. They quit. He didn’t have the cash to buy supplies. Business was hit.

This took a toll on his mental health. He felt watched, monitored. His wife, worried, sent him back to his village in West Bengal for a few months.

The family’s income was down to her wages. But expenses remained constant.

After managing by borrowing for a year, in 2017, it was time to send their 15-year-old daughter to a new school. The school insisted on her having a minor bank account. Familiar with Kotak, the Mitras opened her an account in a nearby HSR branch. The bank took a cheque for Rs 10,000. This was yet another account where they needed to maintain a minimum balance. Another account they didn’t know they had to. Fourth blow.

By mid-2017, the fees and charges came thick and fast from all three accounts.

Rs 354 ($5), monthly, for non-maintenance of the minor account.

Rs 531 ($7), monthly, for non-maintenance of the savings account.

Rs 1,770 ($25), quarterly, for the current account.

Since April 2016, they’ve paid up Rs 22,000 ($300) in charges across the three accounts. More than their current income.

By mid-2017, Mitra had to downsize to his current shop in Sarjapur.

Overall, Mitra could only maintain average monthly savings of about Rs 7,000 ($100), according to Purav Parekh, co-founder of GLIB.ai, a company that uses technology to help users get analytics on their bank statement. The company analysed Mitra’s bank statements on The Ken’s request, with his consent. “Bank charges do not normally exceed 1% of average minimum balance over the course of a year,” said Parekh.

But Mitra has incurred charges more than 100% of his average monthly balance, taking both accounts into consideration, said Parekh.

“We usually monitor maintenance of balance, and if, for successive months, we notice non-maintenance charge, we alert customers,” claims Puneet Kapoor, executive vice-president at Kotak. ”When we notice these charges, we advise the customer to move to a zero-balance account.” Alternatively, if a customer brings it up, they claim to waive the charge and migrate the user to another bank account.

There’s a catch. “We issue [zero-balance] only if someone asks about it [at the time of opening a savings account],” admits Kapoor.

Selling to those who can’t pay: human cost of modern banking

The Ken asked Mitra if he ever went to the bank to contest the fees. He says he couldn’t afford to leave his shop unattended and go away for two hours. And, besides, the prospect of going to such a big bank intimidated him.

The Mitras, despite avoiding using the credit card, had to take it out for their son’s school fees. “And that’s also because his school insisted on paying it digitally, so we decided to use the card,” says Mitra’s wife.

But banks thrive on credit cards. Just look at the IPO prospectus of the country’s second-largest credit card issuer SBI Cards and you’ll know. It made Rs 7,200 crore ($1 billion) in revenue in the financial year ended March 2019 with 50% of its income coming from the interest it earns.

Given credit cards’ importance to a bank’s revenue stream, they are mis-sold, admits a senior banker at a private bank. Kapoor of Kotak Mahindra Bank also admits that Mitra should not have been given a credit card. One year of deposit history is not enough data to give a card.

Multiple Achilles heels

Selling to those who can’t pay: human cost of modern banking

But bank reps aren’t the only ones to missell. When salespersons target those in the mass segment, there are multiple ways they prey on insecurities. They may start with building aspirations, and they may build it up to a situation where the customer needs saving.

Then they play saviour.

In August 2018, a salesperson from Justdial pitched an ad-service to Mitra—‘here’s how your carpentry service can be listed prominently on Justdial in Bengaluru’! Mitra needed to grab some eyeballs for his small Sarjapur business. The cost? Rs 8,000 for the first month plus an Electronic Clearing Service (ECS) mandate, which Mitra signed again without realising. This gave his bank the consent to deduct money from his account automatically every month.

That’s Rs 50,843 ($700) Mitra didn’t expect to pay up. “They told me pay for one month, and if you don’t like it you can cancel,” he says.

A month later, when no new business came in, Mitra says he asked Justdial to terminate the contract. Justdial’s customer care centre claims to have no record of this call or the termination itself.

In just a month, Justdial pinged his account at least six times hoping to dip into the savings anytime he deposited cash. Each ECS request that bounced from the account attracted a Rs 590 penalty from the bank.

Mitra paid ECS penalties worth Rs 3752 ($50) in December 2018, his bank statements show. The recurring ECS requests from Justdial would go on for another five months, long after there was no money left to debit.

Justdial did not respond to questions on their sales method or why they pinged an account multiple times. Kotak Mahindra said, the charges levied for non-maintenance and ECS-return are essentially a “penalty for poor banking behaviour.”

The Mitra family also played right into the hands of other scamsters. As recently as June 2019.

18 days after Mitra’s wife opened a bank account at Vijaya Bank, she got a call from a scammer posing as a bank manager. “He told me because my Aadhaar card was from WestBengal, it won’t work here and he is shutting off my ATM service.” All he needed was the One Time Password (OTP) and her card CVV number to reactivate the ATM service.

Result? Rs 7,000 ($100) gone.

“I knew I’m not supposed to give my ATM pin and OTP, but this man knew all my details, so I was convinced he was from the bank,” she says.

Questions to Vijaya Bank on how details that were confidential to the bank landed in the hands of a scammer went unanswered.

Sales machine

Selling to those who can’t pay: human cost of modern banking

How did one family become the centre of misselling of not one, but all five products that were sold to him?

Kotak Mahindra insists that the account had “no irregularities”. And that there were “regular transactions taking place [with] positive balances in [Mitra’s] savings account with no charges levied for non-maintenance of Average Monthly Balance (AMB)”. “He also had a good credit bureau score. Based on this, after 6 months, we cross-sold him a current account, a credit card, and a life insurance policy in October 2016,” says the bank in a written response to The Ken. “This is not an anomaly,” the bank adds.

And yet, deviations happen. It begins with the sales agents who are on a mission to meet targets laid out by the banks. Much like any FMCG company selling soap. Except here, they are selling some of the most complex financial products. “Sales agents act on the leads received by banks,” says a sales agent who sells credit cards. “The leads can come from anywhere in the city. It is not restricted to one geography,” he says. That explains how Mitra was wooed by agents from different branches.

Incentives drive salespersons. “The incentives can be 40% to 100% of your salary, so the opportunity to earn more is significant,” explains a sales manager at Kotak Mahindra Bank. When it comes to closing a sale, offering information voluntarily can ruin the sale, admitted a branch head at Yes Bank requesting anonymity.

Selling to those who can’t pay: human cost of modern banking

At The Ken, we applied for a credit card to observe the process. The third-party agent representing ICICI Bank, who came to collect the Know Your Customer (KYC) documents and get signatures, failed to bring a brochure with credit card details. Even though the application requires the customer to read the brochure before signing. “It’s all sent over email. We stopped carrying the physical brochure with us long ago,” says the agent. But the email would not be sent to everyone. “They’ll send it to you only if you ask for it,” he says, admitting that there would be customerswho would not be aware of all the details of the product because of this.

So what happens when you don’t have an email address?

In Mitra’s case, the agents just manufactured one. Different fake email IDs for his credit card and life insurance accounts. So Mitra neither got his credit card statements over email nor did he get a physical copy.

When we asked Kotak Mahindra what they do to make sure agents sell the right product, Puneet Kapoor said they train and sensitise the agents to sell the right products. He also said they issue forms in vernacular languages and give a shortened version of the terms and conditions called the ‘most important terms and conditions’, which customers need to read and sign. At a mass level, customers’ signatures are the only check to ensure that they’ve understood what they’re signing up for, he said.

“With deposit products, banks end up incurring major costs, so there is no incentive to missell,” says a senior banking executive. But then again, how far did that savings account take Mitra?

After all, banks are in this for the money. Hence, the costly charges and fees.

Selling to those who can’t pay: human cost of modern banking

The banker quoted above claims banks have no choice but to charge for these products because it is forced to give many services for free. For example, payments transfers using National Electronic Funds Transfer (NEFT) have been made free. Similarly, the government has mandated that banks cannot charge merchants a fee for accepting digital transactions. “Maintaining all this infrastructure is costly. The regulator looks at the benefit for consumers, but we need to run a business too. There are no free lunches,” said the banker.

The other reason the likes of Mitras fall prey is that banking products have been created for the top 30% of the Indian population, says Rajat Singh, head of micro-banking at Ujjivan Bank, a small finance bank, which focuses on the mass market.

No perfect model

Ujjivan is banking to mass market by having no charges for non-maintenance of minimum balance in all its savings accounts. It has no cap on the amount of annual transactions. It offers 6 monthly free ATM withdrawals on other bank’s ATMs. Ujjivan too doesn’t make money on these accounts as it says building banking behavior takes time

Selling to those who can’t pay: human cost of modern banking

While banks continue to focus on profit, Mitras—and those like them—are stuck in this vicious cycle. Save. Lose. Borrow. All they’re counting on is that the next generation, with access to good education, breaks free of this cycle.

This is why when the Mitras got a call with the voice on the other end promising better education for their son, they went with it. They thought it was the school calling, except it was a sales agent from the tuition app Extramarks. The agent knew the name of their son’s school; the company claims to have gathered this through outreach events which they conduct. The Mitras were told that two counsellors would come home and give an evaluation test.

The counsellors came on a Sunday. The test itself was free but the subscription they recommended based on it was not. Not wanting to come in the way of their kid’s education, they paid up the fees. Rs 3,333 ($45).

It is only later that the Mitras realised they had signed up for an annual subscription worth Rs 30,000 ($420) for Extramarks, a tuition app for children. Rs 3,333 was the first EMI.

They called Extramarks to discontinue this EMI, but they could not. Extramarks refused to cancel. Eventually, they got a partial refund of Rs 1,000 ($14).

Karunn Kandoi, a senior executive at Extramarks, told The Ken that the company is aware of the problem of misselling and has set up multiple processes to ensure that the customer is aware of what they are signing up for.

“I’m now convinced that the chances of my money getting stolen from my bank account is higher than if I keep it at home,” says Mitra’s wife, defeated.

MS Sriram, faculty at the Centre for Public Policy at IIM Bangalore, sees the logic in that. “Banking for the poor is overrated. It only makes sense from a data collection perspective and helping make the right policies for that segment. But when it comes to helping [those like Mitra], banking is not going to make a big difference in their lives, unless it is backed up by subsidies,” says the professor.